- Why an Interest Calculator Matters

- Simple Interest vs Compound Interest

- Simple Interest Calculator

- Compound Interest Calculator

- How an Interest Growth Calculator Helps You Plan Better

- Key Features to Look For in an Interest Calculator

- 1. Support for Simple and Compound Calculations

- 2. Flexible Compounding Options

- 3. Recurring Contributions

- 4. Clear Final Balance and Total Interest

- 5. Easy-to-Read Layout

- How to Use an Interest Calculator Effectively

- Common Use Cases for an Interest Calculator

- Saving for a Goal

- Investing for the Future

- Understanding Loan Costs

- Retirement Planning

- Benefits of Using Digital Interest Tools

- Final Thoughts

Interest Calculator: Best Easy Compound & Simple Interest Tool

Interest calculator tools make it much easier to understand how money grows over time, whether you are saving, investing, borrowing, or planning for a financial goal. Instead of manually working through formulas, you can quickly estimate future balances, compare scenarios, and make better decisions with only a few inputs. From basic savings accounts to long-term investments and loans, the right calculator helps turn confusing numbers into clear insights.

When people think about financial planning, they often focus only on the starting amount. In reality, interest rate, time period, and compounding frequency can have an even bigger impact. That is why digital tools have become so useful. A simple calculator can show how small changes in contribution amount or interest rate can significantly affect the final result.

Why an Interest Calculator Matters

An interest calculator is more than a convenience. It is a practical tool for budgeting and decision-making. Whether you are trying to grow savings or understand the cost of borrowing, accurate projections matter.

Here are some common ways people use it:

– Estimate returns on savings accounts

– Compare investment growth over time

– Calculate loan interest

– Plan retirement savings

– Understand how extra contributions affect long-term results

– Check the difference between simple and compound growth

Many people underestimate how powerful interest can be, especially over longer periods. Even a modest rate can create meaningful growth when given enough time. On the other hand, debt can also become much more expensive when interest is not fully understood.

Simple Interest vs Compound Interest

Before choosing the right tool, it helps to understand the two main types of interest.

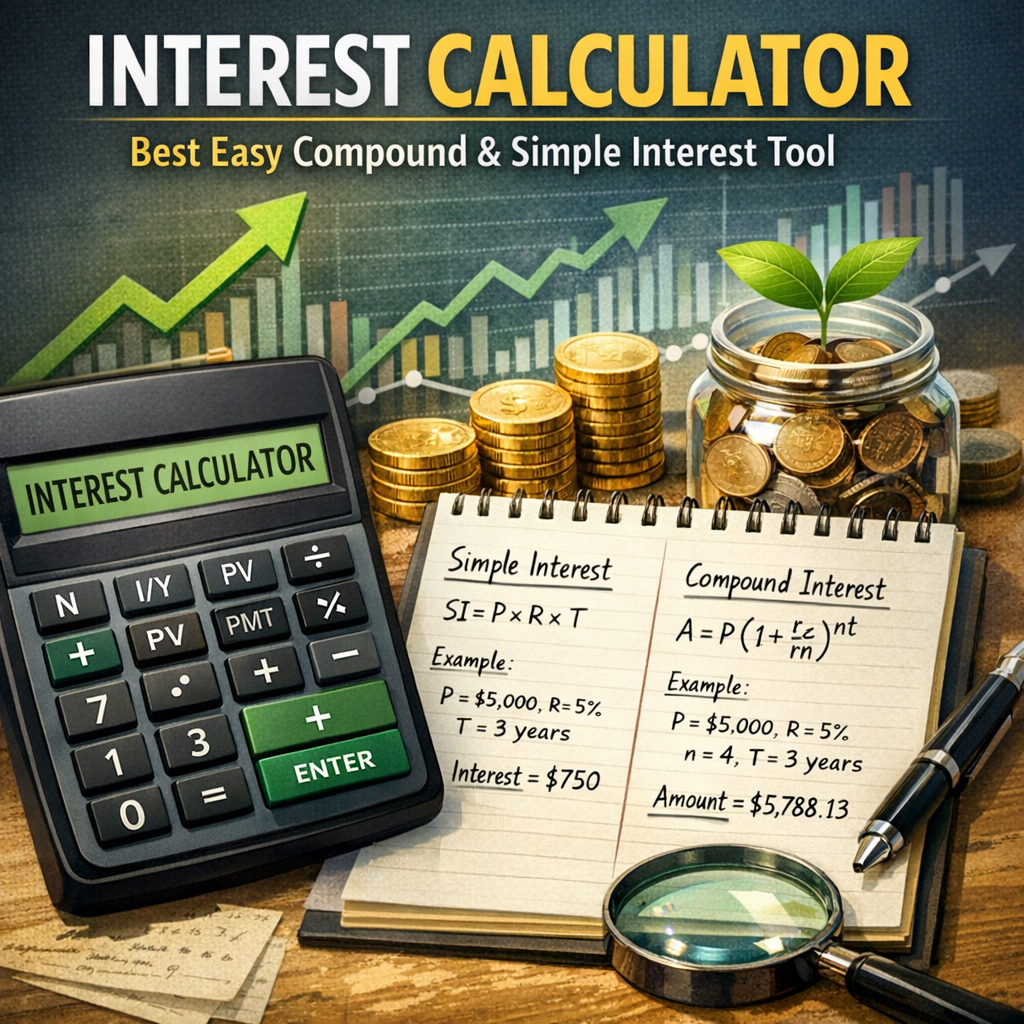

Simple Interest Calculator

A simple interest calculator is used when interest is calculated only on the original principal. That means the interest does not build on previously earned interest. This method is straightforward and often used for certain short-term loans or basic financial examples.

The standard formula is:

Simple Interest = Principal × Rate × Time

For example, if you invest $1,000 at 5% simple interest for 3 years, the interest would be:

$1,000 × 0.05 × 3 = $150

At the end of 3 years, the total amount would be $1,150.

This type of calculation is helpful when you need a quick estimate and the terms are fixed. A simple interest calculator saves time and removes the need to do the math manually.

Compound Interest Calculator

A compound interest calculator is used when interest is added back to the balance, allowing future interest to be earned on both the original amount and the accumulated interest. This is what makes compound growth so powerful.

Unlike simple interest, compounding rewards consistency and patience. The longer money stays invested, the greater the growth potential.

For example, if you invest $1,000 at 5% compounded annually for 3 years:

– Year 1: $1,050

– Year 2: $1,102.50

– Year 3: $1,157.63

That final balance is higher than with simple interest because the interest keeps building on itself.

A compound interest calculator is especially useful for:

– Savings accounts

– Retirement planning

– Long-term investments

– Education funds

– Recurring contribution analysis

How an Interest Growth Calculator Helps You Plan Better

An interest growth calculator focuses on the bigger picture: how your money changes over time. Instead of showing only one final number, many tools also reveal year-by-year growth, contribution impact, and total interest earned.

This makes it easier to answer practical questions like:

– How much will my savings be worth in 10 years?

– What if I add $100 per month?

– How much difference does a 1% higher rate make?

– How often should interest be compounded?

– How quickly can I reach my target amount?

These insights are valuable for beginners and experienced investors alike. A clear growth projection can motivate better saving habits and help you set realistic milestones.

Key Features to Look For in an Interest Calculator

Not all calculators offer the same level of detail. If you want the best experience, look for a tool that includes the following:

1. Support for Simple and Compound Calculations

A useful calculator should allow you to switch between simple interest and compound interest depending on your goal.

2. Flexible Compounding Options

Daily, monthly, quarterly, and annual compounding can lead to different results. A good tool should let you compare them easily.

3. Recurring Contributions

If you regularly add money to savings or investments, this feature is essential. It helps you see the long-term impact of consistent deposits.

4. Clear Final Balance and Total Interest

You should be able to instantly view:

– Initial principal

– Interest earned

– Contributions made

– Ending balance

5. Easy-to-Read Layout

The best financial tools are simple, clean, and beginner-friendly. You should not need advanced math knowledge to use them.

How to Use an Interest Calculator Effectively

Getting useful results depends on entering realistic numbers. Here is a simple process:

1. Enter your starting amount

2. Add the annual interest rate

3. Select the time period

4. Choose simple or compound interest

5. Set compounding frequency if needed

6. Include monthly or yearly contributions if applicable

7. Review the total balance and interest earned

To make better financial choices, try adjusting one factor at a time. For example, compare:

– 5 years vs 10 years

– Monthly contributions of $50 vs $200

– 4% interest vs 6% interest

– Annual compounding vs monthly compounding

These comparisons can reveal just how much time and consistency matter.

Common Use Cases for an Interest Calculator

An interest calculator is helpful in many everyday situations.

Saving for a Goal

If you are building a travel fund, emergency reserve, or home down payment, a calculator can show how long it may take to reach your target.

Investing for the Future

Long-term investing is where compound growth can make the biggest difference. Even small regular contributions can lead to strong results over time.

Understanding Loan Costs

While many people use calculators for savings, they are also useful for debt planning. You can estimate how much interest a loan may generate and how repayment timing affects the total cost.

Retirement Planning

A compound interest calculator can help you estimate how today’s contributions may grow over decades. This is one of the most important uses of any financial planning tool.

Benefits of Using Digital Interest Tools

Using a calculator instead of manual formulas offers several advantages:

– Faster calculations

– Fewer errors

– Easier comparisons

– Better financial confidence

– More informed planning

– Stronger motivation to save or invest

It also helps turn abstract ideas into real numbers. Financial planning often feels overwhelming because it involves future outcomes. A visual or structured calculator makes those outcomes easier to understand.

Final Thoughts

An interest calculator is one of the simplest and most useful tools for managing money wisely. Whether you need a simple interest calculator for basic estimates, a compound interest calculator for long-term projections, or an interest growth calculator to map your financial future, the right tool can save time and improve your decisions.

By understanding how interest works and testing different scenarios, you can make smarter choices about saving, investing, and borrowing. The best results often come from starting early, contributing consistently, and letting time work in your favor. A good calculator does not just provide numbers—it gives you clarity, direction, and a stronger sense of control over your financial goals.